Is Your Internal Audit Communicating for Influence?

By

By

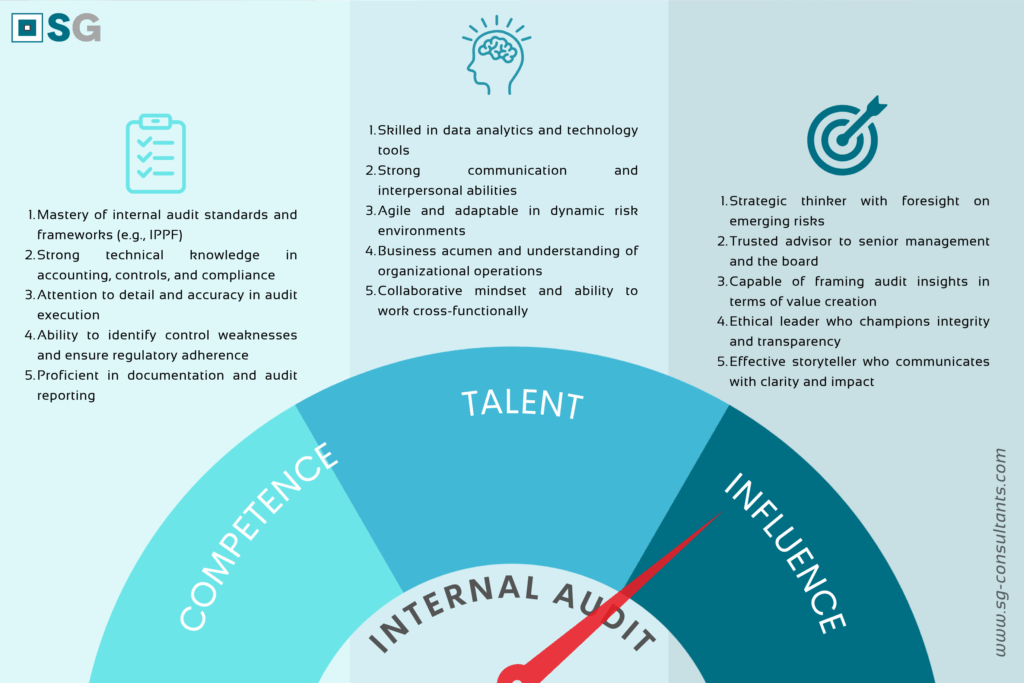

The context of business today is often said to be a ‘dynamic risk environment’! Whatever that means, internal audit functions have over time been expected to do more than identify control weaknesses—today, they are expected to influence decisions, shape strategy, and drive value. This weighs more expectations on the internal auditor, the Chief Audit Executive and the Board Audit Committee over and above the attributes of competence and talent that are due. But, as a point of caution, influence is to be differentiated from charismatic individual traits and it is not a thing of fluke. It is a state of impact arrived at through intentional, strategic communication.

The Global Internal Audit Standards (2025) emphasize that internal auditing must enhance and protect organizational value by providing risk-based, objective assurance, advice, and insight. Easier said than done, this is an audacious statement of purpose. To fulfill this purpose, internal auditors must not only be technically competent and leverage technology for efficiency, but also communicate in ways that resonate, persuade, and inspire action.

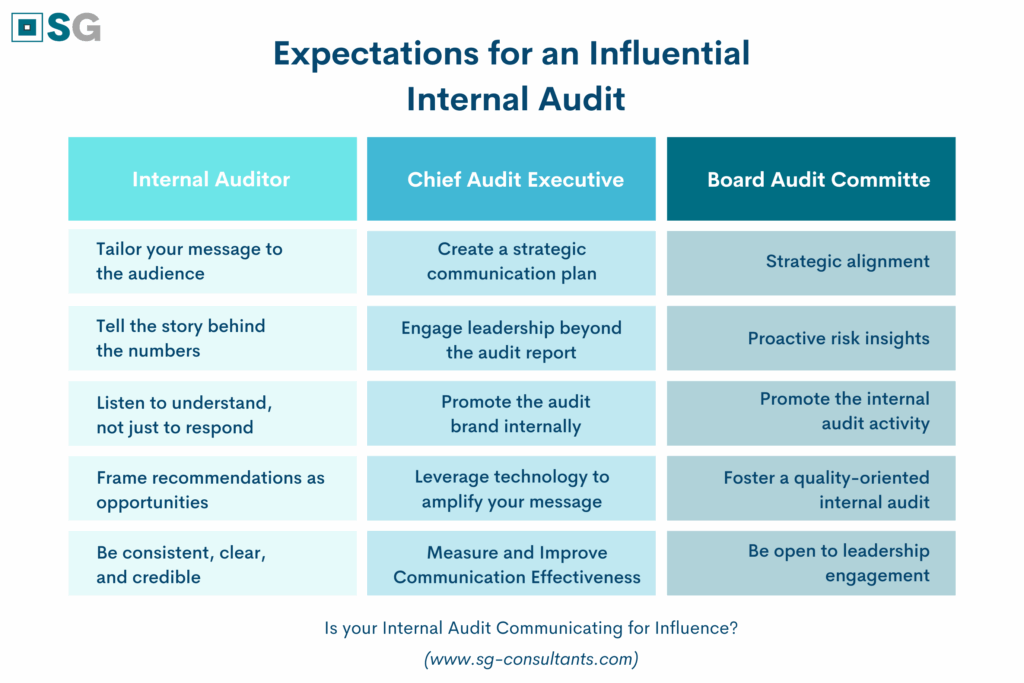

So, how can internal audit communicate for influence? We offer a practical guide with expectations for the internal auditor, the chief audit executive and the board; action-oriented strategies that can drive change and promote organizational value creation.

For the Individual Internal Auditor

- Tailor your message to the audience: There is an extant debate over the futility of long reports and empirical evidence points to the idea that internal audit reports are not sufficiently digested (read) by executives. Directors care about strategic impact; operational managers want practical solutions. Adjust your tone, depth, and format to meet their needs and expectations.

- Tell the story behind the numbers: beyond producing multiple graphs that can leave your audience bewildered, use data storytelling to connect audit findings to business outcomes. This entails some level of critical analysis and creativity. Visuals, analogies, and real-world examples make your message stick.

- Listen to understand, not just to respond: Influence begins with empathy. Per Lenz and Enslin (2025), empathy is the ability to put oneself into someone else’s shoes and to not only understand their position but also to appreciate their feelings. And this is an attitude that fosters openness and collaboration.

- Frame recommendations as opportunities: Instead of focusing on what’s wrong, highlight how improvements can reduce risk, increase efficiency, or support strategic goals. As an internal auditor, it is easy to become cynical, and take pleasure in uncovering and bluntly reporting problems. To strike a balance in perception and increase acceptability, frame recommendations by highlighting the benefits of executing them and opportunity cost of not.

- Be consistent, clear, and credible: Your words carry weight when they are backed by integrity and clarity. Make clear from the planning phase the purpose of the audit and the level of access that would be needed, document and discuss observation as they unforms. Avoid jargon, be concise, and always support your conclusions with evidence. One key that always works: stay on the facts and avoid surprises.

For the Chief Audit Executive:

- Create a strategic communication plan: Clearly identify those who constitute your audience (internally and externally) and define how, when, and to whom audit insights are communicated. As a rule of thumb, it is wise to always anticipate more and react less. Use dashboards, executive summaries, and regular updates to stay visible and relevant.

- Engage leadership beyond the audit report: It is a wild error to think business starts with the audit plan and ends with the follow up of recommendations. Actively build relationships with the board and C-suite through informal briefings, risk updates, and strategic discussions—not just formal audit reports.

- Promote the internal audit brand internally: At a recent conference, a panel speaker used the term “matraquage communicationnel” (communication assault), a term he used to highlight the level of persistence and consistency the CAE must put to work to cement a certain perception of the purpose of internal audit. Use newsletters, success stories, and internal campaigns to position internal audit as a proactive, value-adding partner. Communicate!

- Leverage technology to amplify your message: Use data visualization tools, audit management systems, and real-time reporting to make communication faster, clearer, and more impactful. Technology can often be overlooked; it is your friend and can be a useful servant.

- Measure and Improve Communication Effectiveness: Solicit feedback, track engagement, and refine your approach. The auditee feedback form is often considered that one last formality to close the internal audit. But it should be taken more seriously. See it as an opportunity to improve. Communication is a skill—and like any skill, it improves with practice and reflection.

The expectations from the internal auditor and CAE are often echoed the loudest. However, no matter how competent and experienced internal audit staff are, the internal audit function can hardly fulfill its purpose without the support of the board audit committe.

Board Oversight Expectations for a More Influential Internal Audit:

- Strategic alignment: Internal audit should align its priorities with the organization’s strategic goals. The Global Internal Audit Standards drives deep on the idea of an internal audit strategy (Domain IV, Standard 9.2), as a means to supporting the strategic objectives and success of the organization. Internal audit should have a long-term plan that transcends the annual audit plan.

- Proactive risk insights: The board expects internal audit to identify emerging risks and provide foresight. At a recent internal audit conference, a speaker asked: “If the CFAF were to be devalued today, what rescue plans have you designed for your organizations?” A question that left the audience in an awkward silence. Proactive risk-thinking also entails asking the bold questions, considering those risks that most would think elusive, farfetched and beyond the pay grade of the CAE.

- Promote the internal audit activity: position and resource the internal audit function as fully empowered to provide a critical check for management, a knowledgeable provider of assurance and a revered consultant.

- Foster a quality-oriented internal audit: ‘Quality-oriented audit committees beget quality-oriented internal audit activities.’ Its is vital for the Board audit committee to build metrics of assessment of the quality of its internal audit, and ideally, these metrics should trickle town into the performance assessment criteria of the CAE and Internal Auditors. Go beyond performance on the audit plan, look into the Quality Assurance and Improvement Program.

- Be open to leadership engagement: The board and executive team should maintain regular, meaningful engagement with internal audit leaders. Engaging in an open, transparent relationship is key for influence.

Final Thoughts

Influence is not about authority—it’s about connection, clarity, and credibility. Internal auditors who communicate with purpose and empathy can shift perceptions, shape decisions, and truly fulfill their mission of enhancing and protecting organizational value.

So, ask yourself: Is your internal audit communicating for influence—or just for compliance?