Internal Audit in the Risk Assurance Puzzle: From Risk Identification to Strategic Oversight.

By

By

Introduction

Internal auditors are tasked with evaluating the design and operational effectiveness of internal controls and reporting their findings to management and the board. In doing so, internal audit contributes a vital piece to the broader assurance landscape—helping stakeholders gain confidence that the organization is progressing towards its strategic objectives.

The prevailing paradigm for internal audit is ‘risk-based auditing’ — and rightly so. But what does it truly mean to “audit at the speed of risk,” as Richard Chambers famously puts it? How do we move from identifying risks to auditing processes, and how does internal audit fit into the broader risk assurance framework? This article walks you through a step-by-step approach to understanding internal audit’s role—not just as a final checkpoint, but as an integral part of a coordinated, organization-wide risk assurance process. Internal audit is one player among many: management, risk and compliance functions, investigations, and governance all contribute to the assurance puzzle.

We’ll explore how risk is managed throughout the organization, how that feeds into a solid risk-based internal audit plan, who the key participants are in the organization-wide risk assurance puzzle, and how to build an adapted risk assurance map to improve coordination and optimize assurance efforts across the enterprise.

1. Understanding Organizational Risk Management

1. Understanding Organizational Risk Management

Organization-wide risk management is best understood through the structured process outlined in ISO 31000. Although often presented linearly, this process is inherently iterative and dynamic, requiring continuous engagement and refinement. The key stages include:

- Risk Identification: Proactively and reactively identifying risks and documenting them in the organization’s risk register and risk universe.

- Risk Assessment: Classifying risks based on established criteria (e.g., ownership, description) and evaluating their severity using measures of risk appetite, tolerance, and capacity.

- Risk Response: Defining and implementing appropriate mitigation strategies to reduce the severity or likelihood of identified risks.

- Risk Monitoring: Continuously reviewing the status of known risks and the effectiveness of mitigation plans.

- Risk Communication: Ensuring timely and accurate communication of risk-related information—such as emerging risks, escalation reports, and review findings—to senior management and the board.

A vital output of this process is the risk register, which catalogs risks in a structured format, and the risk universe, which represents the full spectrum of risks the organization may face. However, effective risk management must begin with a clear understanding of the organization’s current position, its mission and vision, and its strategic objectives. Anything that threatens the achievement of these objectives constitutes a strategic risk—often represented by the top 10 or 20 risks in the register.

2. Crafting a Risk-Based Internal Audit Plan…Strategy

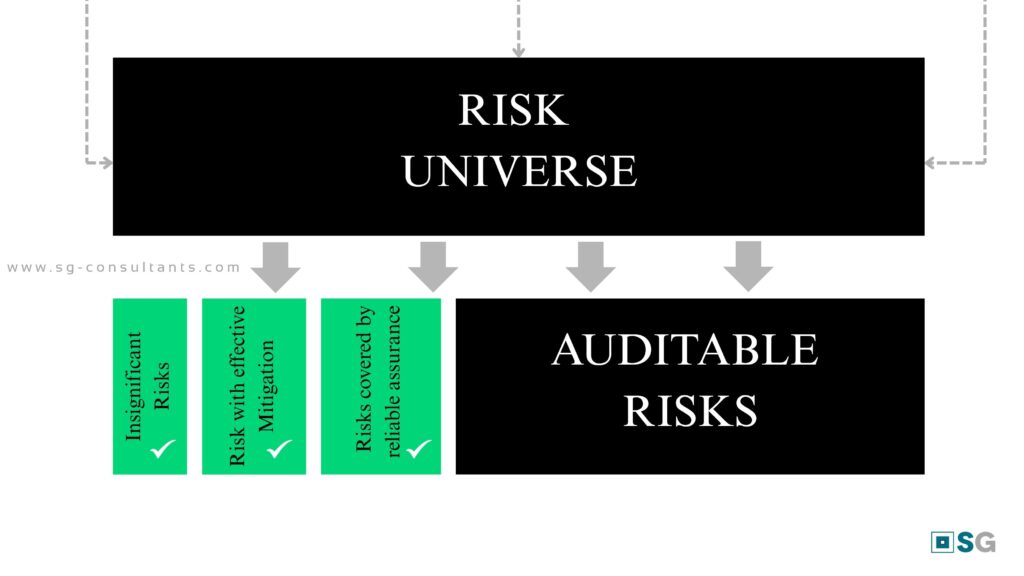

The risk universe encompasses all potential risks and processes that internal audit could consider in its planning. However, not all risks warrant inclusion in the audit plan—this is where strategic filtering becomes essential. To develop a focused and effective internal audit strategy, the audit team should:

- Exclude Insignificant Risks: Internal audit resources are limited and should be directed toward areas where assurance will have the greatest impact.

- Exclude Significant Risks with Effective Mitigation: Where risk reviews and control monitoring confirm that mitigation strategies are working effectively, internal audit may deprioritize these areas.

- Exclude Risks Covered by Other Assurance Providers: The Chief Audit Executive (CAE) should coordinate with other internal and external assurance providers to understand their coverage and avoid duplication. Internal audit should focus on areas where assurance is lacking or unreliable.

After filtering the risk universe, the remaining risks should be aligned with board and senior management priorities. The result is a refined set of auditable risks, which the CAE should assess against available resources—financial, technical, and human.

This strategic approach ensures that internal audit remains focused on the most significant risks, coordinates effectively with other assurance functions, and contributes meaningfully to the organization’s overall risk assurance framework.

3. Mapping the Risk Assurance Ecosystem

With the risk management landscape now defined, it is essential to identify the roles played by each assurance provider within the broader risk assurance puzzle. A practical way to do this is by aligning the Three Lines Model with the responsibilities of each actor in the risk assurance process.

First Line: Operational Management

- Responsibilities: Own and manage risks, identify emerging risks, implement internal controls, and execute risk mitigation plans.

Second Line: Oversight and Support Functions

- Risk Management: Coordinates enterprise-wide risk management, monitors the implementation of risk response plans, maintains the risk register, and ensures the risk universe is regularly updated.

- QHSE, Finance, and Legal: Manage specific risk domains (e.g., health and safety, financial accuracy, legal liability) and report on the effectiveness of related controls and mitigation strategies.

- Compliance: Oversees compliance-related risks within the ethical, legal, and regulatory frameworks governing the organization.

- Internal Control: Continuously monitors the operational effectiveness of internal controls and the implementation of risk responses.

- Investigations: Examines reported incidents or control failures with potential fraud implications, determines root causes, and recommends corrective actions.

Third Line: Internal Audit

- Responsibilities: Provides independent assurance on the effectiveness of governance, risk management, and internal control processes across the first and second lines.

External Assurance Providers:

- External Consultants and Auditors: Offer independent, specialized assurance on specific risk areas, often requiring technical or industry-specific expertise.

The involvement of multiple assurance providers highlights the complexity of the risk assurance ecosystem. Without proper coordination, responsibilities may overlap, leading to inefficiencies or assurance gaps. This underscores the need for strong board oversight and a deliberate effort to align assurance activities with the organization’s priorities and available resources.

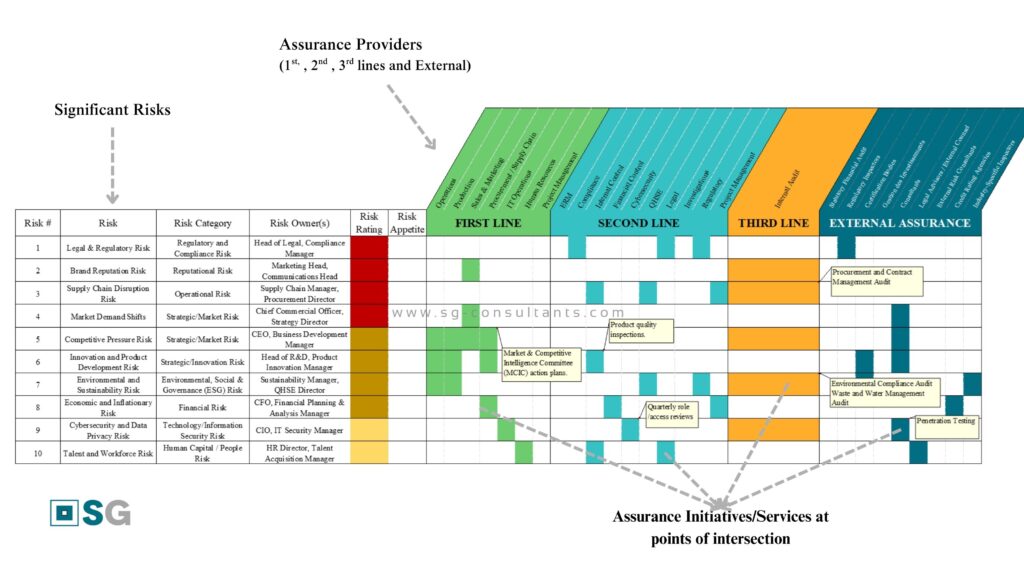

4. Building a Risk Assurance Map for Strategic Coordination

A Risk Assurance Map is a powerful tool for coordinating assurance efforts across the organization. It visually aligns significant risk exposures (on one axis) with assurance providers (on the other), offering a clear view of who is providing assurance on what, and where gaps or overlaps exist.

In the context of annual audit planning—or more broadly, annual risk assurance planning—the intersections on the map indicate whether a risk is being addressed, by whom, and through what type of activity (e.g., audit, review, advisory).

Benefits of a Risk Assurance Map

The RAM gives the board and senior management panoramic visibility on a number of points:

- Identifies assurance gaps: Highlights significant risks that lack adequate assurance coverage.

- Reveals duplication: Shows where multiple providers are addressing the same risk, prompting opportunities to streamline efforts.

- Optimizes resources: Helps the CAE and the audit committee allocate assurance resources more effectively across the organization.

For an editable basic spreadsheet template to guide you towards building your risk assurance map, and advise on your risk assurance projects, you can reach me on [email protected].

Making the Map Interactive

To make your risk assurance map more user friendlt, the map can be made interactive by incorporating:

- Color coding to indicate the level or type of assurance (e.g., audit vs. advisory).

- Pop-ups or tooltips showing planned dates, responsible teams, and status updates.

- Links to supporting documentation such as audit reports, risk assessments, or remediation plans.

Getting the map done

To get the risk assurance map done, the CAE can leverage a range of tools—from simple spreadsheet applications like Excel and Google Sheets to more advanced platforms such as Power BI, Tableau and GRC systems (e.g., MetricStream, RSA Archer), and collaborative tools like Airtable or Smartsheet.

Advanced tools can enhance the map’s interactivity, enable real-time updates, and support better visualization and coordination of assurance activities. Selecting the right tool depends on your organization’s size, the complexity of its operations, and maturity of its risk management and assurance framework.

Conclusion: Move towards Integrated and Strategic Risk Assurance

As organizations navigate increasingly complex risk landscapes, the role of internal audit must evolve from isolated evaluations to strategic participation in a coordinated risk assurance framework. By understanding how risks are managed, crafting a risk-based audit strategy, mapping the assurance ecosystem, and leveraging tools like the Risk Assurance Map, internal audit can position itself as a central player in delivering meaningful assurance to the board and senior management.

This integrated approach not only enhances the effectiveness of assurance activities but also ensures that resources are deployed where they matter most—on the risks that threaten the achievement of strategic objectives. Ultimately, internal audit’s value lies not just in identifying control weaknesses, but in helping the organization see the full picture of risk and assurance, and act on it with clarity and confidence.

Should you have any experience using risk assurance maps and other assurance coordination tools, kindly share your experiences in the comment section.

Thank you.