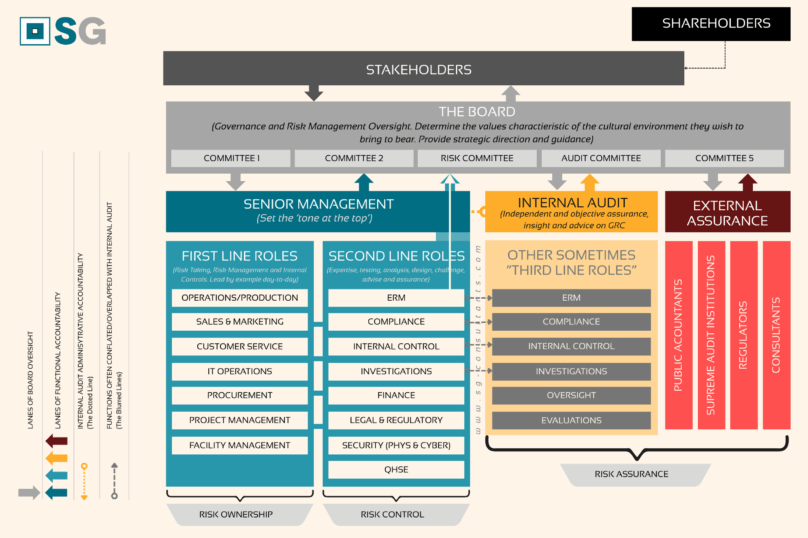

Above, the Three Lines Model, tweaked to reflect reigning concerns, and responsibilities for risk oversight, ownership, control and assurance.

Amid ongoing debates about the practicality and relevance of the Three Lines Model, critics have recently gained renewed momentum—especially following the announcement by the IIA CEO in the latest edition of Internal Auditor magazine that the Institute will be “Reimagining the Three Lines.”

—————————————

Longstanding criticisms of the model include:

Oversimplification: The model presents a linear structure that does not adequately reflect the complexity and dynamism of modern organizations.

Silo Emphasis: It may reinforce functional silos, hindering collaboration and information sharing among assurance providers.

Ambiguous Role Definitions: The model assumes clear-cut distinctions between second line functions and internal audit. In practice, roles such as risk management, compliance, internal control, and investigations often overlap or are conflated with internal audit.

Moreover, in many organizations, Chief Audit Executives (CAEs) are tasked with overseeing second line functions such as risk management and compliance—often in the name of alignment and cost optimization. This arrangement, while practical in some contexts, raises concerns about the independence and objectivity of internal audit.

—————————————

Despite these valid concerns, we believe the Three Lines Model remains not only relevant but a gold standard for corporate governance, for several key reasons:

Scalability: The model can be adapted to suit the maturity level of an organization’s internal control environment.

Flexibility: It accommodates local governance frameworks and regulatory requirements.

Preservation of Independence: It provides a structured space for internal audit—not one of privilege, but of independence, which is essential for credible risk assurance.

The limitations often attributed to the model are more reflective of imperfect governance practices than of the model itself. When faithfully applied, the Three Lines Model continues to deliver on its promise of structured, coordinated, and effective assurance.

—————————————

The limitations often attributed to the model are more reflective of imperfect governance practices than of the model itself. When faithfully applied, the Three Lines Model continues to deliver on its promise of structured, coordinated, and effective assurance.

We offer a detailed illustration of the model that emphasizes:

The agency relationship between ownership, stakeholders, and the board.

The integrated relationship between first and second line functions.

The lines of oversight and reporting to board-level committees.

The third line roles that are often housed under the CAE but should not compromise internal audit’s independence.

The distinction between internal and external assurance, both often positioned within the third line but serving different purposes.

—————————————

While the model has been criticized for being too theoretical and insufficiently adaptable to contemporary governance realities, it remains a valuable framework. Organizations should not adopt it as an off-the-shelf solution, but rather as a strategic guide to strengthening their risk assurance architecture.

We anticipate that the IIA’s reimagined model will retain its core structure and name, while reinforcing safeguards for independence and objectivity—principles that are foundational to effective governance.

—————————————

At SG Consultants, we support businesses and professionals in structuring their assurance frameworks by integrating the principles of the Three Lines Model. Our tailored approach helps you clarify roles, optimize synergies between functions, and build governance that aligns with the specific challenges of your sector. Contact us to turn your ambitions into a robust and sustainable control architecture.

By

By